FINANCIAL MANAGEMENT COURSEWORK

REPORT FOR COLEFAX GROUP ACQUISITION

I. Academic Justification

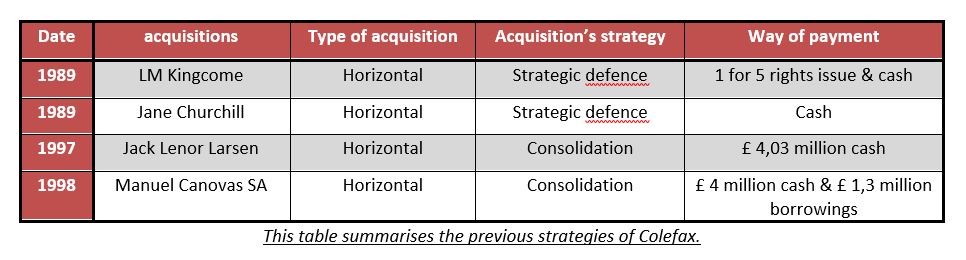

Colefax Group has made 4 acquisitions during the last 25 years: two in 1989, one in 1997 and the last in 1998.

The first two acquisitions of 1989 (Jane Churchill Ltd and LM Kingcome) are part of the fourth stage. A downward trend had characterised M&As before this period which means that we have made few mergers before. Indeed, the US credit crisis of 1966 and the fall in stock prices had profoundly affected the world economy. The French economist Clement Juglar identified that the global economy is led by the alternation of three cycles of 9 or 11 years which have become shorter with the globalisation. According to his theory of cycles, there would be a boom phase corresponding to the economic growth and stages of mergers and acquisitions favoured by the good development of the economic system and by the willingness of companies to reach out to the previous economic crisis; a phase called a ultrafast crisis produced by the loss of the companies’ objectives and extensive stock market speculation; and finally a phase of worldwide depression corresponding to the period of economic crisis (Juglar, 1862). Thus, the acquisitions of our group are eased by the 3D’s - Deregulation, Disintermediation and Decompartmentalisation - , which are also made thanks to the growth stage in order to acquire a taller size and prominence. Colefax wanted to grow its business and become bigger on the market through M&A activities which can bring several competitive advantages by these pre-emptive actions due to a strategic defence (Colefax annual report, 2011). Jane Churchill Ltd was also acquired to consolidate the UK Colefax’s power on this market and to avoid a competition between the two companies. LM Kingcome was acquired in the same year by the strategic defence in order to reinforce its range of new products.

During the fifth stage, an economic growth period following a crisis, Colefax group chose this period to acquired Jack Lenor Larsen (1997) and Manuel Canovas SA (1998) to focus on the long-term and strategic deal to obtain a growth of its business. It is why the company has expanded through a number of strategic acquisitions over the last 15 years. Those two acquisitions were made in a consolidation goal to act as an economic trigger due to technological, financial or regulatory impetus (Mitchell and Mulherin, 1996 – Harford, 2005) and allowed these following outcomes: cash flow margin, asset turnover, research and development expenses, capital expenditures and return on assets (Harford, 2005).

Our sector has been hit particularly hard by the subprime crisis in 2007; we are now in the growth stage and it seems an opportunity to consolidate our sector, realise profit and expand us by a new acquisition by our group. This acquisition will probably mark the beginning of a new stage of growth - the sixth stage – in the area of the property market and home furnishment.

II. Commercial Justification

The 4 acquisitions of our group are horizontal takeovers which are common during this period. Indeed, during the fourth and the fifth stage, there were numerous horizontal acquisitions in specific industries (e.g. consumers’ goods industry). A horizontal takeover is possible only between two companies which operate in the same industry and at a similar stage of production. Indeed, all of those were in the designer and distributor of luxury furnishing fabrics and wallpapers.

LM Kingcome was acquired in order to obtain its know-how especially in Sofas which were an immediate success and a competitive advantage for Colefax and, moreover, facilitated the R&D development. Indeed, Colefax acquire an innovation and technological competence of another UK company. Now, Jane Churchill and LM Kingcome are two of our subsidiaries: Jane Churchill is one of the fabrics five brands and LM Kingcome one of the range of furniture.

By acquiring Jack Lenor Larsen in 1997 and Manuel Canovas SA in 1998, Colefax group created an economy of scale and synergy in R&D area, design, distribution and marketing area. Our company had decided to improve the sales of the Larsen group by consolidating Larsen distribution, by decreasing its cost in the US and to expand in the European market (Financial Times, 1997). So Jack Lenor Larsen became one of the fabrics five brands of Colefax thanks to its contemporary woven textile competences. In July 1998, sales in the US were helped by this acquisition for £4,3 million. Thus, Colefax’s sales represented 58% of trade sales in the US in 1997. Thanks to this, Colefax group grew up 40% (Financial Times, 1998).

Manuel Canovas SA concluded in 1998 an agreement with Colefax group to become the last of its subsidiaries during this period. Our CEO of Colefax group, David Green, decided this acquisition to increase its turnover and to expand his company abroad. We noticed in October 1998 a rise of 29% in sales of Colefax to £31,2 million (£24,1 million) helped by its latest acquisition with the French company and the shares closed up 5p at 71p (Bilefsky, 1999).

Our CEO, David Green, has decided to do those four acquisitions in growth stages to reinforce his company, to realise synergistic benefits and the diversification of its products’ range, and finally to expand and conquered other foreign markets – especially with the Manuel Canovas acquisition in order to conquer the French market. However, since 2000s with the coming of the European protectionism, it has become more expensive and hardest to realise agreements between countries. This is also a decision to consolidate our sector. The choice of the CEO to do horizontal acquisitions was not without the intention to increase market share and hence increase a company’s ability to earn monopoly profits (Colefax annual report, 2011).

Colefax group entries on new markets (the US and France) thanks to its acquisition and although the firm has suffered the economic crisis, it maintained its place and improve its sales due to current abroad penetration. An internal growth would be too slow in a globalisation world that is the reason why Colefax group chose the acquisition ways a more efficient route to its expansion.

In 2007, the subprime crisis touched the property and consequently our sector of home furnishment. It created weakness of housing market and housing transaction. Thus, to fight the crisis of the decoration and furniture sector, a new acquisition in the coming day could be an opportunity to recover a competitive position on the market, especially on the UK market to consolidate our first position on this market and create a sustainable advantage. Moreover, as David Backwell said in the Financial Times of October 1998, whatever the growth prospects, a merger with another small company would rekindle the interest sparked by the disposal, which prompted a 40 per cent rise in the shares during April 1998. There are two different groups in a similar line of business in wallpaper and fabrics, which can acquire Walker Greenbank, one is our company Colefax & Fowler, valued at £22m in 1998. (Backwell D., 1998)

Thus, with the same commercial strategy, we want to realise a horizontal takeover with Walker Greenbank which works in the same sector at the same degree of production. Walker Greenbank can also become one of our new subsidiaries with its good reputation on the market.

This acquisition can be created in order to combined the wealth of the two companies (PV X+Y)>(PVX+PVY) and generated economic gains (to reduce production costs) thanks to the best competitiveness of the new company on the market (Watson and Head 2007, p. 313). It will create a synergy thanks to the combination of their outputs which will become more important than the sum of their separate outputs. As we have seen before it forms an economy of scale because the scale of operations is larger after a takeover.

III. Financial Justification

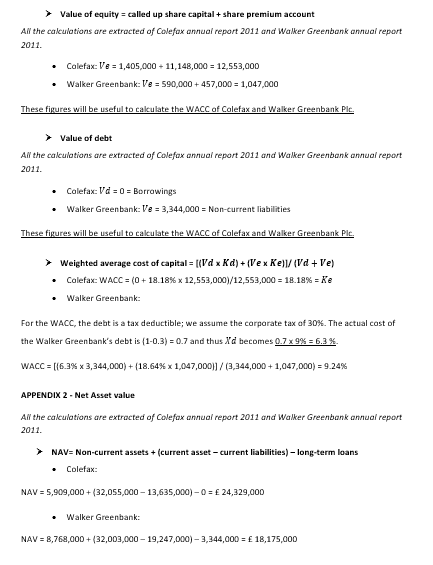

To consolidate our sector, it seems profitable to realise the acquisition of Walker Greenbank Company because its turnover is around £65,000,000 per year and only a little lower than its of our firm which is of £75,000,000 this year and we work in the same activity sector. Furthermore, we can allow us to realise expenditures or a borrowing to bind a contract between our group and the Walker Greenbank Company as we have no long-term debt due to the repayments of our previous loans. But according to Miller and Modigliani, if we contract borrowings, it does not impact on the WACC of Colefax because the WACC remains unchanged whatever the employed financial leverage of debt (Miller and Modigliani, 1958).

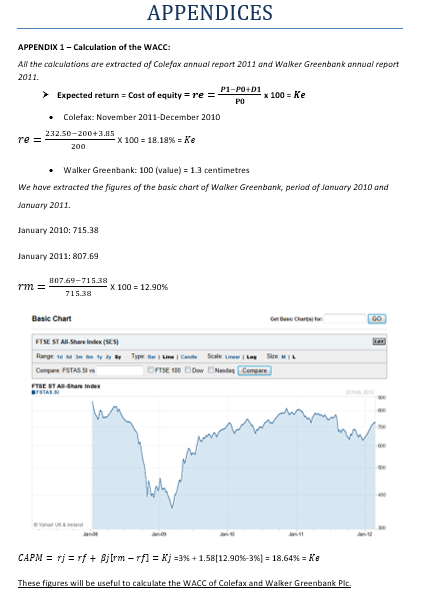

To calculate, the WACC, we need to determine the cost of equity, the cost of debt, the value of equity and the value of debt of our company and of Walker Greenbank (APPENDIX 1).

It is the return that stockholders require for a company.

It is used to measure a company's size and helps investors to diversify their investments across companies of different sizes and different levels of risk.

Our group has free debt whereas Walker Greenbank has borrowings so contracted a long-term debt as investment capital.

The WACC is the after-tax weighted average annual rate of return expected by shareholders and creditors, in return for their investment. The weighted average has the weights equal the percentage of each type of financing in a firm’s overall financial structure (Megginson and al. 2008, p. 341). We use after tax WACC formula because typically interest payments to bondholders are tax deductible (Megginson and al. 2008, p. 341).

For the WACC, the debt is a tax deductible; we assume the corporate tax of 30%. The actual cost of the Walker Greenbank’s debt is (1-0.3) = 0.7 and thus the cost of debt becomes 0.7 x 9% = 6.3 %.

We can notice that the WACC of Colefax is double that of Walker Greenbank because our company has a pretty high WACC. Thus, if Colefax acquires Walker Greenbank, its WACC will decrease with increasing its amount of debt financing; after the acquisition of Walker Greenbank, the WACC of Colefax should fall from 18% to 14% because the WACC is not static. The weighting can change but the costs of different sources of finance can change too and it is the case if we acquire Walker Greenbank (Watson and Head 2007, p. 257). As the market value of the company depends of its WACC, it creates a higher Nat Present Value of its future cash flows and so a higher market value.

The WACC represents the Investment appraisal: the discount factor is derived on the WACC and the safety factor and it causes greater opportunities for the business. So it can increase the number of possible investment possibilities.

If we decide to acquire Walker Greenbank, this acquisition type will be a type-2 acquisition because by combining the WACC of Walker Greenbank, the outcome alters that of the final entity, WACC of Colefax. This will result in a definite change to the discount factor being applied to prospective future cash flows and increase the Net Present Value.

IV. Valuation

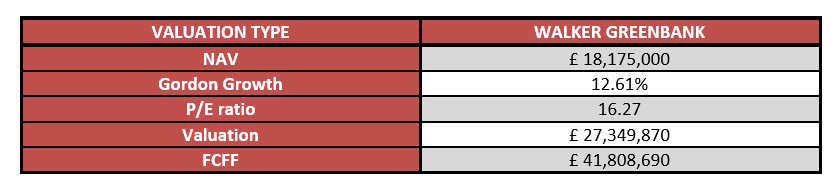

The Net Asset value of Walker Greenbank of 18,175,000 is the minimum sum that we can propose to the acquisition of Walker Greenbank Plc. The Net Asset Value offers only the lower limit for the target company’s value (Watson and Head 2007, p. 323).The Net Asset value of Walker Greenbank of 18,175,000 is the minimum sum that we can propose to the acquisition of Walker Greenbank Plc. The Net Asset Value offers only the lower limit for the target company’s value (Watson and Head 2007, p. 323).

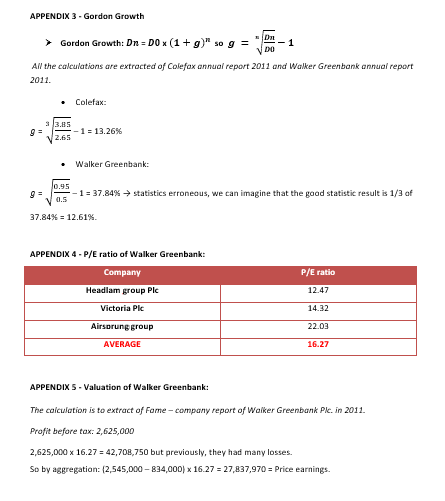

The value of a company can be estimated by using the Gordon growth model to calculate the present value of future dividends accruing to its shares. But as the statistics seems erroneous, we can just guess the right statistic and so we must pay attention to the P/E ratio to evaluate the valuation of Walker Greenbank (Watson and Head 2007, p. 326).

It shows how much an investor is prepared to pay for a Greenbank’s shares. But it informs to the confidence of investors in the expected future performance of a company. The higher of this P/E ratio, the more confident the market is that future earnings will increase. So we can be confident if we acquire Walker Greenbank because this company have a high P/E ratio (Watson and Head 2007, p. 53).

We have adjusted the cost to stop window dressing which it tries to artificially boost the profit. We balanced last year with this year to have more representative figures. The price earnings is the price that we want to propose to Walker Greenbank Company to obtain its firm. But we must wait for approval by Walker Greenbank treasury.

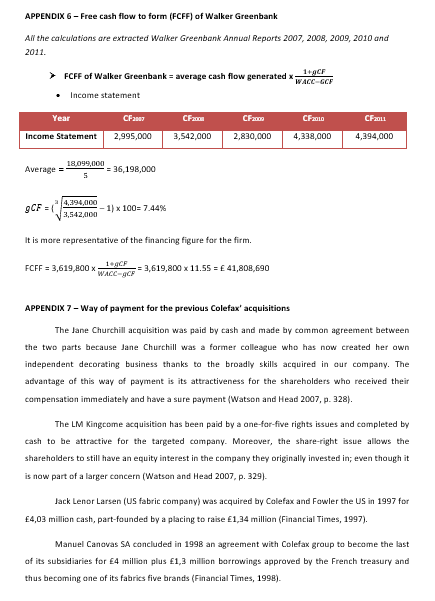

The FCFF of Walker Greenbank of £ 41,808,690 is the profit that we can expect after the acquisition of Walker Greenbank Plc. and it seems an efficient acquisition because the expected benefit is higher than the sum that we expected to buy Walker Greenbank for. It is also the maximum sum which our group can invest to buy Walker Greenbank without expected any deficit (Watson and Head 2007, p. 325).

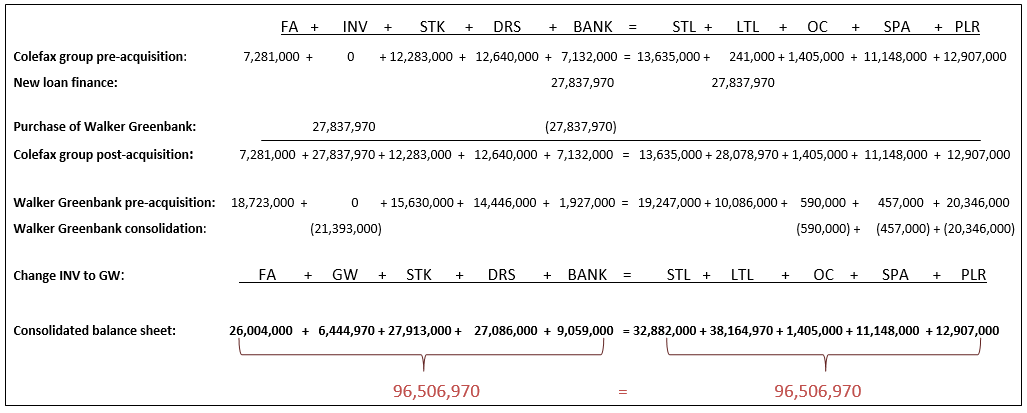

The purchase of Walker Greenbank achieves our strategy; it impacted Goodwill of £ 6,000,000. The ‘Goodwill’ created when a firm is acquired by another company for more than the acquired firm's book value is the premium over book value which represents the higher market value of intangible assets such as patents, copyrights and trademarks, as well as brand relationships that are not accounted for at all. Charges arising from goodwill impairment can have a dramatic effect on reported earnings. Thus, we can say that if we realise this acquisition for £ 27,000,000 we obtain Goodwill of £ 6,000,000 which is the most important value of Walker Greenbank. (Megginson et al. 2008, p. 37)

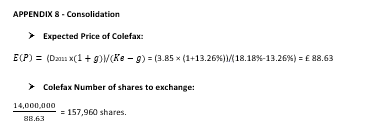

We decide to pay 13,000,000 in cash and 14,000,000 in shares because we want to propose £ 27,000,000 to Walker Greenbank to obtain its firm. It is a mix between cash and shares offers according our previous strategy (APPENDIX 7). We decide to give 157,960 shares to Walker Greenbank to conclude this agreement.